How did herd behaviour contribute to the Global Financial Crisis?

By Syuan Ruei Chang

The Global Financial Crisis (GFC) of 2008–2009 was a watershed event for economies all around the world. Initially beginning in the US, the GFC began with the bursting of the US housing bubble and a massive default on subprime housing loans, triggering a series of events which included the collapse of major investment bank Lehman Brothers. The impacts of the GFC extended beyond the financial sectors and beyond the borders of the United States, and spurred a series of recessions worldwide, forcing massive government bailouts and generating calls for greater regulation of the financial industry.

Why did the crisis occur?

One of the most puzzling questions remains — Why did the crisis occur? The blame of the crisis lies not on a single individual, but by the culmination of mistakes by many well-educated, experienced, and reputable professionals. In understanding the causes of the GFC, later economists and academics, with the benefit of hindsight, point to certain ‘tell-tale’ signs of an impending collapse. The question therefore points to why so many of these trained individuals — from regulators to bankers to economists — failed to recognise the signs at the time. To that end, an understanding of the behavioural sciences may be useful in explaining why so many unsound investment decisions had been made, and why the trend continued until the bubble popped.

A model of herd behaviour

‘Herd behaviour’ is a phenomenon observed by the behavioural sciences that offers a potentially compelling explanation for why mistakes were made during the GFC. A simplified version of Banerjee’s (1992) model, where a group of n risk-neutral investors invest in one of the k stocks, best exemplifies herd behaviour by solving for the Bayesian-Nash Equilibrium[1] [2] . A Bayesian game is one where agents have imperfect information about how other players will behave, and based on this incomplete information, agents maximise the expected utility of their actions. In this model, there is only one correct investment, which rewards the investor, while all other options will yield a payoff of zero. All the agents in this model want to make the correct investment and enjoy the payoff, but none of them know which investment is the correct one.

In this game, some of the players will receive a signal telling them which investment is the ‘correct’ one. However, there is no guarantee that the signal received by the investor is correct, and the probability of the signal pointing the investor to the ‘correct’ investment is uniformly distributed between the values of [0,1]. Players in this model make their decisions in sequence, where they can observe the decisions made by all previous investors, but not whether the previous players received a signal. Each player in this game will make their decision based on the information encoded in their personal signal (if they have received one), and the choices made by the previous players. Once all the players have made their decision, the correct investment will be revealed, and the participants who made the correct decisions will be rewarded.

Banerjee’s model (described in greater detail in the appendix) shows that herd behaviour may compel agents to abandon their own private information to ‘follow the crowd’, even if previous players made their decisions without any prior information whatsoever. This model indicates a curious outcome, where the ability for players to observe how others behave can lead to a less — rather than more — optimal outcome. Due to herding, a better outcome could potentially be achieved if agents were unable to observe what others are doing. As such, in the context of the financial market, the act of herding — where agents suppress personal beliefs and signals to mimic the decisions of others — is said to have the ability of increasing price volatility and amplifying the magnitudes of the ‘ups’ and ‘downs’ of the market.

In most herding literature, herd behaviour can be considered as either spurious or intentional. Spurious herding occurs when individuals facing the same problem are exposed to identical stimulus and information, resulting in them making the same decision. Spurious herding can be considered an efficient outcome, as it involves the rational response of individuals. On the other hand, intentional herding describes a situation where an agent deviates from the original decision, but only because they have learnt what other agents have chosen. The outcome of intentional herding can be considered as inefficient, contributing to greater degree of market volatility than in a market without intentional herding. To understand the linkages between herding and its effect on the Global Financial Crisis, we can examine the mechanisms by which herding occurs and link them to phenomena observed during the GFC.

One example of irrational herding is trading on noise. This describes traders who make investment decisions by following signals with little impact on the fundamental value of the asset, resulting in these investors trading ‘irrationally’. Trading on noise is a behaviour difficult to eliminate from the market, as it is still possible for noise traders to make correct investment decisions, even when the reasoning behind their choice of investment may seem unsound or nonsensical. Their success induces them to take bigger, resulting in potentially bigger compensations. Noise traders who made incorrect investment decisions and then leave the market are replaced by new ones, perpetuating the presence of ‘noise trading’ in the market. On the other hand, Golec (1997) points to the possibility of rational noise-trading, where investors with short-term investment horizons speculate on market movements driven by noise traders, and use their ‘trading on noise’ to turn a profit for themselves.

Another approach toward irrational herding focuses on the behavioural aspect. Under irrational psychological and sociological influences, investors may deviate from their original actions based on their own signals, and instead change their investment decisions to ‘follow the herd’. Behavioural economist Robert Shiller identifies the phenomenon of ‘irrational exuberance’, which can explain herding in the housing market bubble. Driven by excessive optimism about future housing prices, the signals and beliefs of an individual are altered by what he dubbed the ‘social contagion of boom thinking’. With asset value growth lending credibility to ‘new era’ stories, this wave of optimism provided an enticing illusion that the boom would be unprecedented — in that the swelling in prices would not lead to a bust. The herd behaviour by consumers to take out subprime housing loans and bankers to give them out created a scale of investment on subprime mortgages that were sufficiently high to trigger a full-blown crisis. The psychological and behavioural explanations for herding extended to the behaviour of credit rates, policymakers, and regulators in identifying risk of financial instruments (Grosse, 2017). Swayed by a general sense of exuberance and optimism, the ability for these stakeholders to analyse risk and identify unsustainable investments were hamstrung. Believing that ‘growth will continue’ spurred the different stakeholders to act not according to their own signals, but to follow what the herd is doing, contributing to the creation of an unsustainable price rise and the eventual bursting of the bubble.

However, herd behaviour is not confined to irrational agents, and the act of herding can be justified with rational behaviour. ‘Information cascade’ is a form of information-based herding which represents a situation where participants discard their private information in favour of ‘following the herd’. In markets with poor or incomplete information, or those with a great degree of asymmetric information, there is evidence to suggest that the tendency for investors to herd is more pronounced. Conversely, more transparent markets are said to diminish herd behaviour (Alhaj-Yaseen, 2019). In markets such as the markets for complex financial assets, the dubious and asymmetric information associated with financial markets during the GFC — and observed and scrutinised in hindsight — provides a sound explanation behind why herding occurred.

Other examples of rational herding behaviour that explains the behaviour of investors include insurance against underperformance and reputation. Rajan (2006) identifies the incentive for fund managers to herd and buy stocks included as an index, as it provides a benchmark to excuse the poor performances of a manager. Herding reduces the risk of them appearing to be underperforming, which would have significant implications on their customer base. Graham (1999) also identifies reputational reasons for why herding occurs among observers, such as publishers of investment newsletters. By herding, these observers can enjoy positive externalities from acting in a group and making similar predictions, where reputable analysts are willing to herd in order to maintain their pay and prestige.

Herd behaviour in the Global Financial Crisis extends beyond the confines of a national country. Economou (2018) suggests the presence of cross-market herd behaviour, where a crisis in one country causes the stock markets of another country to herd in a similar direction, spreading the crisis globally. Empirical evidence suggests the presence of cross-market herding in stock markets in Brazil, Chile, Mexico, China and Hong Kong towards the US market (Zheng et al. 2010). The effect of cross-market herding eliminates the benefits of international diversification, introducing a new source of risk outside the control of domestic markets.

Difficulties in empirical research

However, even though herding may seem pervasive and intuitive, supporting the hypothesis with empirical evidence is much more challenging. In the financial market, detecting and finding herd behaviour is difficult, and the evidence for herd behaviour, especially prior to the GFC, is particularly inconclusive. The results of studies are heavily predicated on the methodologies adopted, as well as the time and markets studied. For example, Demirer and Kutan (2005) found a lack of herding behaviour in the Chinese stock market, though Tan et al. (2008) finds evidence to the contrary. Meanwhile, Economou et al. (2011) found mixed evidence of herding within the four southern European markets he studied, with evidence in favour of herding in Greece and Italy, mixed in Portugal and none in Spain.

Much of the challenges in detecting herd behaviour lies in the methodology used to detect ‘herding’. Studies of herding rely on ‘clustering’ — which observes how the behaviour of individuals are grouped together. This methodology may be problematic, as it may fail to account for true herd behaviour by failing to differentiate spurious and intentional herding — the former implying a potentially efficient market outcome and the latter representing unnecessary volatility. In addition, to accurately detect herd behaviour, one would also need to know the private information that was discarded by the agent and its outcome, which is a piece of information difficult to obtain.

Within the timeframe of the GFC, several studies do find empirical evidence in favour of herd behaviour in stock markets around the world. Mobarek, Mollah and Keasey (2014) find that herding effects are insignificant during normal times, though they become more pronounced during crises such as the GFC and the later Eurozone Crisis. Meanwhile, Angela-Maria, Maria and Miruna (2015) investigated herding behaviour in Central and Eastern Europe (CEE) stock markets between 2003 and 2013 and found evidence of herding behaviour in four out of the ten analysed countries. Kabir (2017) finds evidence in favour of herd behaviour while analysing the US financial industry. However, even for a period as turbulent as the GFC, there is no unanimous consensus on herding — and Economou et al. (2011) found no evidence that herding effects were intensified due to the crisis in the four markets he analysed.

Capturing herd behaviour is a challenging task, exacerbated by the difficulty of distinguishing between different types of herding. While the mechanism may seem intuitive, the linkage between irrational herd behaviour and market movement leading up to and during the GFC is not immediately clear. For example, Kabir (2017), by distinguishing between fundamental measures of herding and non-fundamental ones, finds that herding in the US market tends to be more ‘spurious’ in nature for commercial and investment banks. This suggests that the similarity in decision-making by market players may not be representative of irrational, signal-abandoning behaviour, but rather the fact that a similar stimulant encouraged similar agents to act in similar fashions.

Conclusion

Despite the difficulty of capturing herding, it remains an important consideration for market movements, even beyond the timeframe of the Global Financial Crisis. An interesting phenomenon for consideration beyond the scope of this discussion would be the rise of cryptocurrency. Unlike traditional currencies where central banks have a say in determining and managing their values, cryptocurrencies see large fluctuations in prices and invite speculative traders. The cryptocurrency market has become another market that researchers of herd behaviour look out for, showing the importance of the discussion surrounding herd behaviour, even beyond the GFC. It is evident that the value arising from understanding herd behaviour will only increase with time.

When does herding occur, or does it even occur? And how does it tie into market booms and busts? To that end, more investigation is required. Nevertheless, the greater incorporation of psychology and behavioural sciences with finance will undoubtedly be useful for governments and policymakers alike. By understanding herd behaviour, incentives can be redesigned to reduce the herd effect, and perhaps allow us to avoid another catastrophe like the Global Financial Crisis.

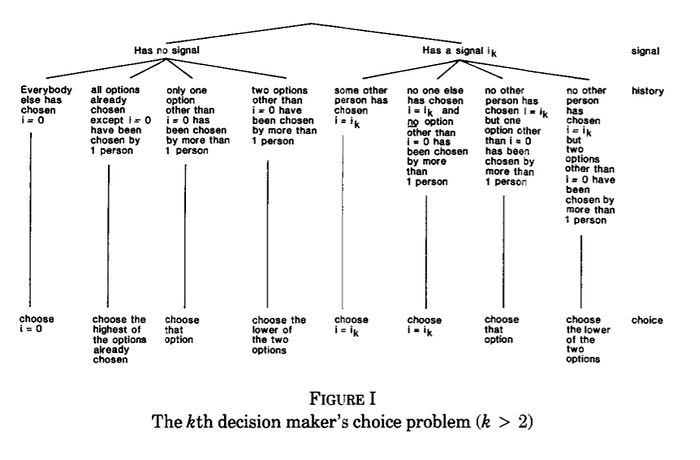

Appendix

Decision-making Logic of Banerjee’s Model

Players in this game are assumed to make their decisions in this way:

- If an investor has no signals, and all preceding individuals have chosen “i=0” (which in this game, is guaranteed to be the ‘wrong’ investment), he will choose the same option as the preceding investors

- If an investor is indifferent between choosing his own signal and following the choice made by another investor, he will choose to follow his own signal

- If an investor is indifferent between the choices others have made, he will choose to follow the investment decision with the greatest value of i

The behaviour of the first few players is described as below:

- If the first player has a signal, he will follow his own signal; if he does not have a signal, he will invest in the ‘wrong’ investment (i = 0), which minimises misinformation in this model

- If the second player has no signal, he will follow the first player’s choice; if the second player has a signal, he will follow his own signal over that of the other player’s

- The third player is faced with four potential scenarios:

- If the third player has no signal, and the two previous players made the same choice, he will follow their choices

- If the third player has no signal, and the two previous players made different choice, he will choose the investment with the highest value of i (and therefore, will not herd at the guaranteed incorrect option ‘i=0’)

- If the third player has a signal, he will always follow his own signal, unless both preceding players made the same investment that is neither i=0 nor the decision suggested by his own signal

- If the third player has a signal, and this decision matches the decision made by one or both preceding players, he will always follow that signal

Diagrammatically, we have the following representation:

Banerjee’s model illustrates the idea that while the first two players will follow their own signals if they have one, there is no guarantee that subsequent players will do the same. If the first two players choose the same option, subsequent players will abandon their private information in favour of following the herd. Notably, such a result can also be observed even if the first two players make different choices. The first player without a signal will choose the option with the highest value of i among those that have already been chosen, and all subsequent decision makers (regardless of whether they have a signal) will follow said choice, unless their signal points them to another option that is already chosen. As such, herding at an incorrect option will always occur, with an exception being made for two cases. The first scenario where herding does not occur involves the first decision-maker (k = 1) having a signal that leads him to the correct choice. Meanwhile, the second scenario involves a subsequent player (k>1) with a signal making the correct choice, but this must occur only before the first player without a signal makes their choice.

This article is written by Syuan Ruei Chang (Research Associate, Economic Research).

Bibliography:

Angela-Maria, Filip, et al. “An Empirical Investigation of Herding Behavior in CEE Stock Markets under the Global Financial Crisis.” Procedia Economics and Finance, Elsevier, 28 Aug. 2015, www.sciencedirect.com/science/article/pii/S2212567115007455.

Banerjee, Abhijit V. “Simple Model of Herd Behavior*.” OUP Academic, Oxford University Press, 1 Aug. 1992, academic.oup.com/qje/article-abstract/107/3/797/1873520.

Bikhchandani, Sushil, et al. “A Theory of Fads, Fashion, Custom, and Cultural Change as Informational Cascades.” Journal of Political Economy, 1 Oct. 1992, www.journals.uchicago.edu/doi/10.1086/261849.

Chiang, Thomas C., and Dazhi Zheng. “An Empirical Analysis of Herd Behavior in Global Stock Markets.” Journal of Banking & Finance, North-Holland, 4 Jan. 2010, www.sciencedirect.com/science/article/pii/S0378426609003409.

Cipriani, Marco, and Antonio Guarino. “Estimating a Structural Model of Herd Behavior in Financial Markets.” American Economic Review, www.aeaweb.org/articles?id=10.1257/aer.104.1.224.

“Does Asymmetric Information Drive Herding? An Empirical Analysis.” Taylor & Francis, 22 Mar. 2019, www.tandfonline.com/doi/full/10.1080/15427560.2019.1573822.

Economou, Fotini, et al. “Cross-Country Effects in Herding Behaviour: Evidence from Four South European Markets.” Journal of International Financial Markets, Institutions and Money, North-Holland, 8 Feb. 2011, www.sciencedirect.com/science/article/pii/S1042443111000060.

Economou, Fotini. “Investors’ Fear and Herding in the Stock Market.” Taylor & Francis, 9 Feb. 2018, www.tandfonline.com/doi/full/10.1080/00036846.2018.1436145.

Golec, Joseph H. “Herding on Noise: The Case of Johnson Redbook’s Weekly Retail Sales Data.” SSRN, 5 Nov. 1997, papers.ssrn.com/sol3/papers.cfm?abstract_id=11250.

Graham, John R. “Herding among Investment Newsletters: Theory and Evidence.” Wiley Online Library, John Wiley & Sons, Ltd, 6 May 2003, www.onlinelibrary.wiley.com/doi/abs/10.1111/0022-1082.00103.

Grosse, Robert. “The Global Financial Crisis-Market Misconduct and Regulation from a Behavioral View.” Research in International Business and Finance, Elsevier, 6 May 2017, www.sciencedirect.com/science/article/abs/pii/S0275531917300223.

“IMF Staff Papers — Volume 47, Number 3, 2001 Herd Behavior in Financial Markets By Sushil Bikhchandani and Sunil Sharma.” International Monetary Fund, www.imf.org/External/Pubs/FT/staffp/2001/01/bikhchan.htm.

Kabir, M. Humayun. “Did Investors Herd during the Financial Crisis? Evidence from the US Financial Industry.” Wiley Online Library, John Wiley & Sons, Ltd, 14 July 2017, onlinelibrary.wiley.com/doi/full/10.1111/irfi.12140.

Kutan, Ali M, and Riza Demirer. Does Herding Behavior Exist in Chinese Stock Markets? (2005). Journal of International Financial Markets Institutions and Money, 15 Aug. 2005, citeseerx.ist.psu.edu/viewdoc/summary?doi=10.1.1.690.5848.

McDonald, Ian M. “The Global Financial Crisis and Behavioural Economics*.” Wiley Online Library, John Wiley & Sons, Ltd, 16 Dec. 2009, onlinelibrary.wiley.com/doi/full/10.1111/j.1759–3441.2009.00026.x.

Mobarek, Asma, et al. “A Cross-Country Analysis of Herd Behavior in Europe.” Journal of International Financial Markets, Institutions and Money, North-Holland, 8 June 2014, www.sciencedirect.com/science/article/pii/S1042443114000651.

Rajan, Raghuram G. “Has Finance Made the World Riskier?” Wiley Online Library, John Wiley & Sons, Ltd, 10 Aug. 2006, onlinelibrary.wiley.com/doi/abs/10.1111/j.1468–036X.2006.00330.x.

Shiller, Robert J. The Subprime Solution. Princeton Univ. Press, 2008.

Spyrou, Spyros. “Herding in Financial Markets: a Review of the Literature.” Review of Behavioral Finance, Emerald Group Publishing Limited, 25 Nov. 2013, www.emerald.com/insight/content/doi/10.1108/RBF-02-2013-0009/full/html.

Tan, Lin, et al. “Herding Behavior in Chinese Stock Markets: An Examination of A and B Shares.” Pacific-Basin Finance Journal, North-Holland, 4 May 2007, www.sciencedirect.com/science/article/pii/S0927538X07000236.

Tharchen, Thinley. How Can Behavioural Finance Help Us in Better … 2012, www.iiste.org/Journals/index.php/EJBM/article/download/1501/1433.